April is typically recognized as Financial Literacy Month, but how often do we really stop and smell the roses? The roses, in this case, being the financial knowledge that we can take with us into May and beyond.

The pandemic has certainly given us a new perspective when it comes to looking at finances and cutting out unnecessary spending. In our recent survey we set out to look at consumer habits and clear up some confusion leading into this year’s Financial Literacy Month.

Some of our key takeaways:

- Almost half of the survey respondents (47%) are currently paying interest on credit card debt.

- Nearly 1/4 of those surveyed have made at least one late payment since the start of 2020, with another 4% unsure if they had or not.

- Over 23% of those surveyed have had to get a new credit card due to credit card fraud or stolen credit card information since the start of 2020.

We also asked respondents questions about common credit score misconceptions, finding out that:

- Sixty-six percent of respondents thought that income has an impact on credit scores(it doesn’t!).

- Twenty-eight percent of respondents said that closing a credit card is good for your credit scores (not true!).

- A whopping 85% of people answered that they think credit scores are included on credit reports (we hate to break it to them, but that is also untrue!).

Debt, Interest, and Late Payments

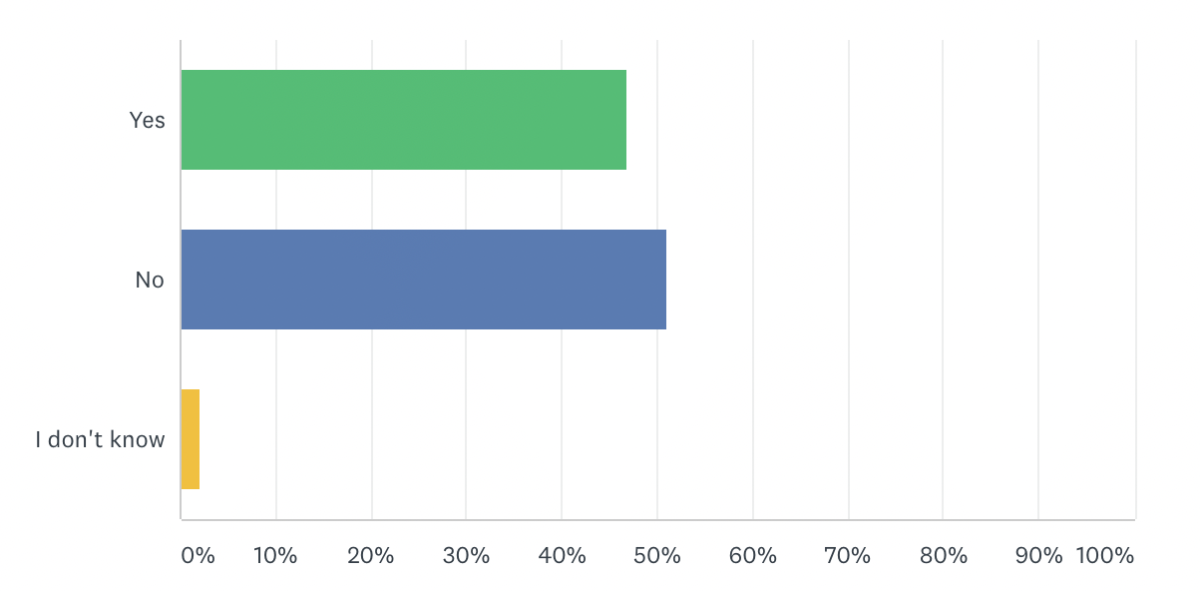

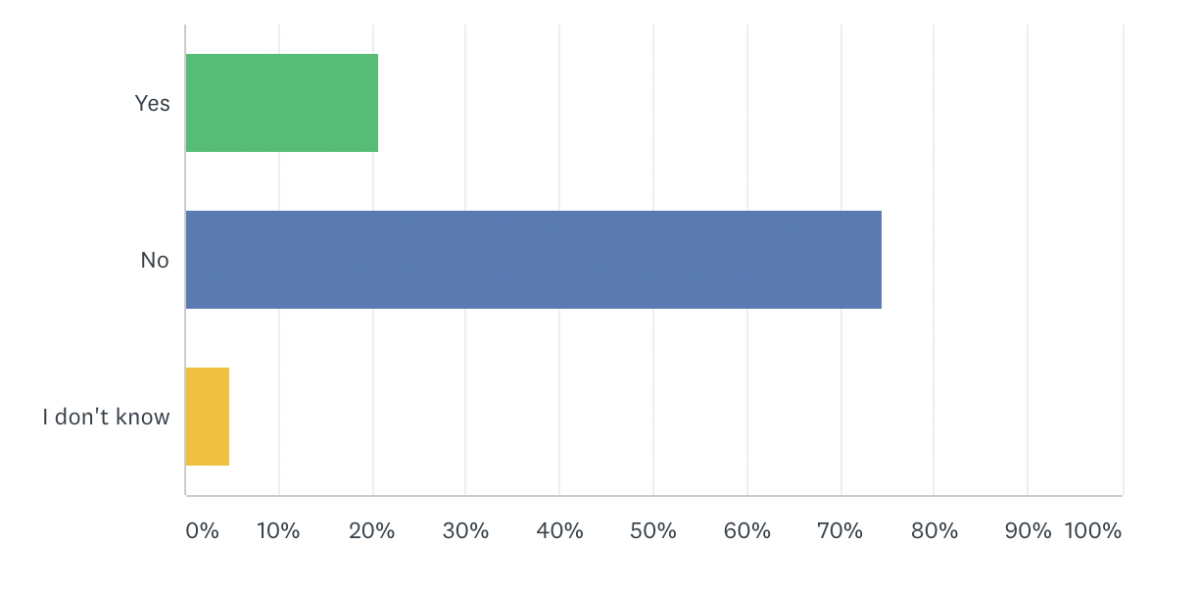

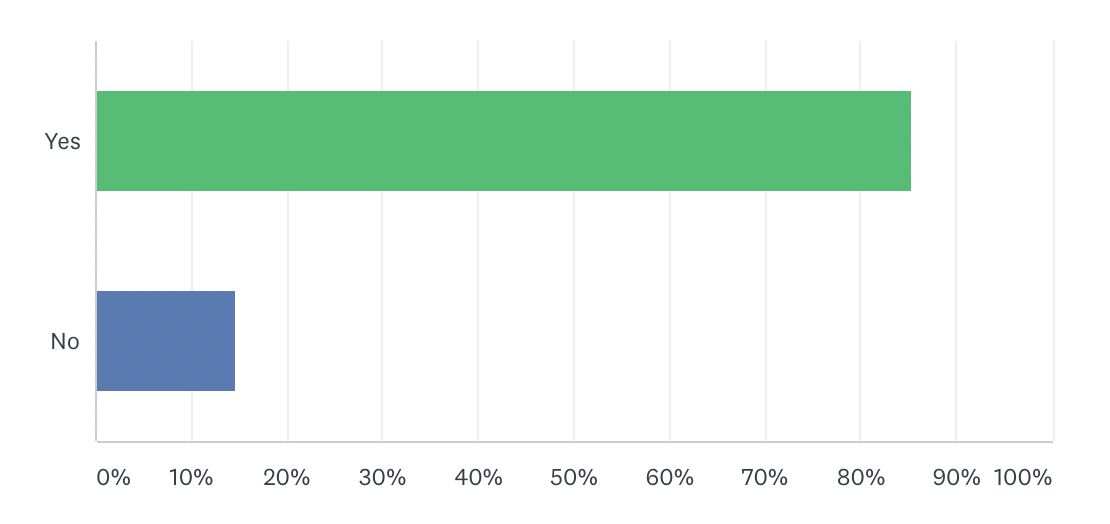

Are you currently paying interest (finance charges) on any credit card debt?

- Yes: 46.80%

- No: 51.12%

- I don’t know: 2.08%

Almost half of survey respondents are letting a chunk of their money go down the drain because of interest charges. Credit card interest rates, on average, are higher than on other types of debt. Do everything you can to avoid paying interest on credit cards altogether.

Start by not charging more to your credit card than you can pay off by the due date — treat it more like a debit card. Most credit cards have a grace period, which means as long as you pay the full statement balance each month by the due date, you’ll avoid interest charges on purchases.

While many people understand the debt and interest charges they’re responsible for, according to our survey, there’s a small percentage of people (2%) who don’t.

That’s an easy problem to fix. Check your monthly credit card statements for your balances, the interest rates of your balances, and the interest charges you’ve been paying. You can see your statements online via your credit card issuer’s website, or have them mailed to you.

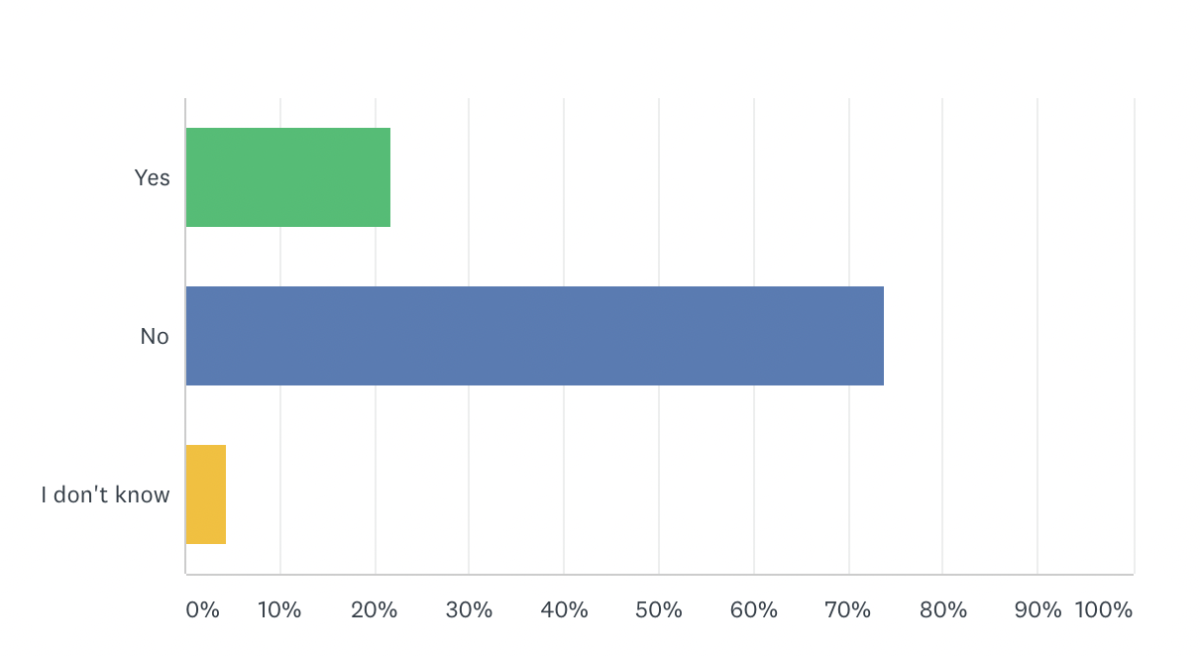

Have you made any late payments that were reported on your credit reports since the start of 2020?

- Yes: 21.79%

- No: 73.85%

- I don’t know: 4.37%

When times are tough, many feel pressure to prioritize one payment over another, which could lead to late payments. Although payments usually have to be at least 30 days late before they’re reported to credit bureaus, late payments can then remain on your credit reports for up to seven years. This can be devastating to your credit scores.

Always try to pay your statement balances in full every month. If that’s impossible, make at least the minimum payment due on time each month to avoid damage to your credit scores. Try to make the biggest payments possible to reduce the amount of interest you’re charged. This will help you get out of debt quicker over time.

Credit Card Security

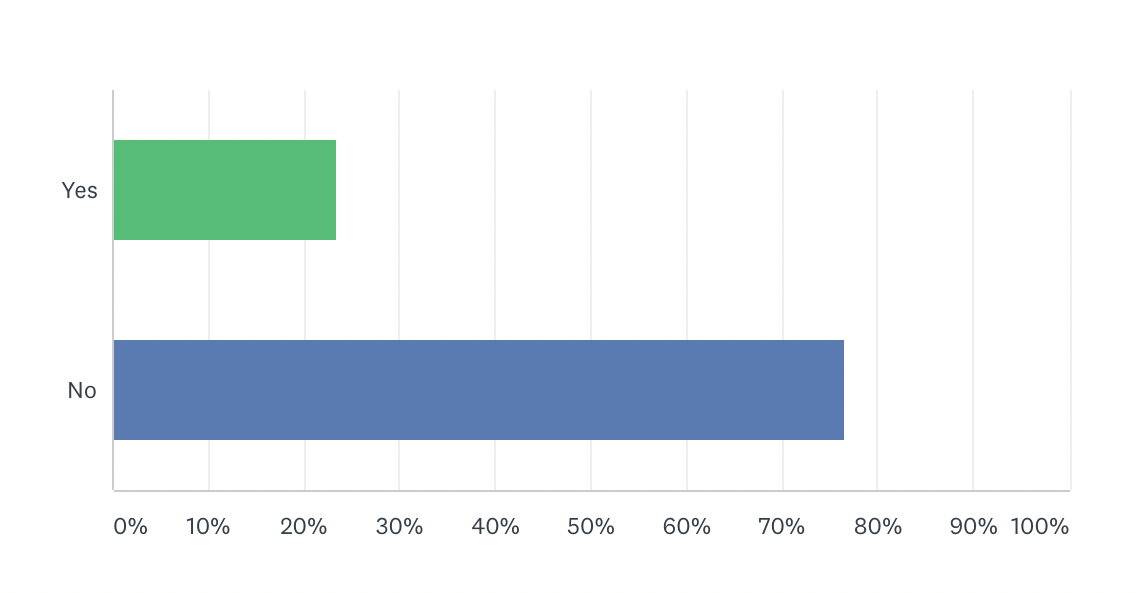

Have you received a new credit card since the start of 2020 due to credit card fraud or stolen credit card information?

- Yes: 23.47%

- No: 76.53%

Alarmingly, over 23% of survey respondents had to receive a new credit card due to either fraud or stolen credit card information. Fraud and identity theft are ever-increasing problems, with each state seeing a significant increase in identity theft reports in 2020, and they can be difficult to identify unless you monitor your bank accounts, card accounts, and credit reports regularly.

In addition to reviewing your accounts and credit reports to look for unauthorized activity, take preventative steps to stop it from happening. Using a mobile or digital wallet for purchases is a great starting point. Some credit card companies also offer virtual credit card numbers, which are digital versions of credit cards that typically feature different card numbers and expiration dates. They can be used online or by phone to help protect your actual account details.

Here are some simple first lines of defense for combating fraud:

- Shop online at trusted merchants only: Look for a lock symbol and “https” in the website URL to make sure it is secure beforehand.

- Don’t make transactions on open networks: Never enter your credit card number when using unsecured public WiFi networks if you’re not sure whether or not the website is secure.

- Don’t share your number with unverified representatives: If you didn’t initiate the phone call or email, don’t give out any personal or financial information.

- Don’t post your personal information publicly: Don’t email your card number, post photos of your credit card, or recite information out loud with strangers within earshot.

If you have serious concerns about identity theft or fraudulent activity, freezing all three of your credit reports is a strong protective measure you can take.

Have you ever frozen any of your credit reports?

- Yes: 20.68%

- No: 74.49%

- I don’t know: 4.83%

Nearly 75% of those surveyed have never frozen their credit reports, but with fraud and identity theft on the rise, it could be a good idea.

Credit freezes prevent lenders from opening new credit accounts in your name, by preventing the credit bureaus from sharing your credit reports with any person or entity (they block hard credit inquiries). The freeze will last until you unfreeze (or thaw) your reports; you’ll have to do that if you want to apply for new credit.

Credit freezes don’t affect your credit scores in any way, positive or negative, nor prevent you from receiving pre-qualified credit offers (since these come from soft inquiries).

If you’re looking for a less strict way to protect your credit, consider a fraud alert, which is basically a minor version of a credit freeze. With fraud alerts placed on your credit reports, lenders have to verify your identity before issuing any credit card or loan in your name, giving you a chance to confirm the request before it goes through.

Unlike credit freezes, fraud alerts don’t completely stop lenders from extending credit in your name, just adding an extra verification step instead.

Understanding Credit Scores

In 2019, we conducted a survey to understand some basic credit score misconceptions, and from our current survey, it’s clear there is still confusion when it comes to credit scores.

Do you think income has an impact on your credit scores?

- Yes: 65.97%

- No: 34.03%

Sixty-six percent of survey respondents thought that income was a factor in determining your credit scores, an increase of 5 percentage points from when we asked the same question in 2019.

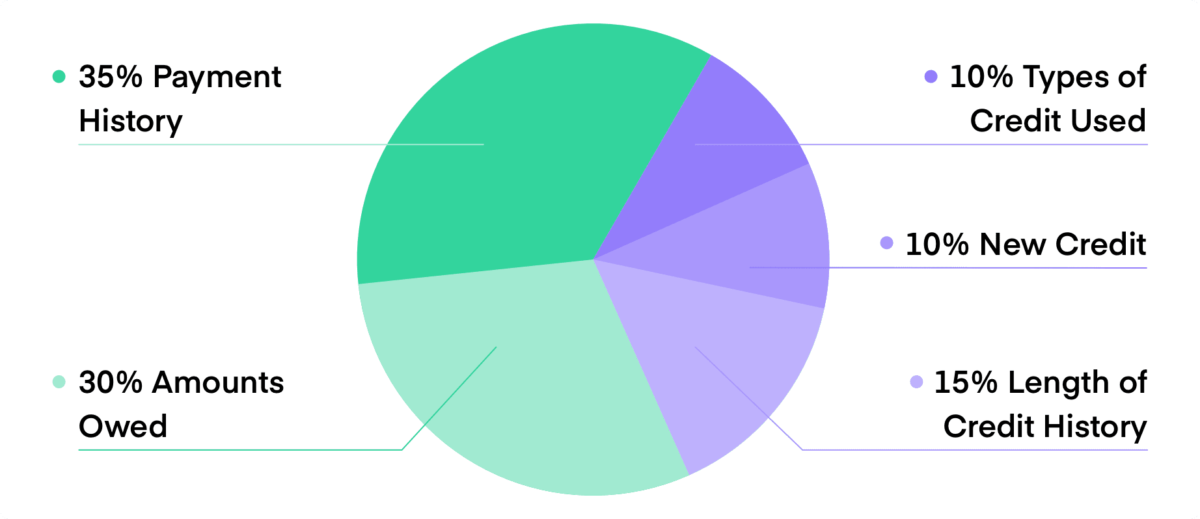

While there are many factors that go into your credit scores, income is not one of them. Payment history, credit card debt, and the length of your credit history all play important roles, but the amount of money you make doesn’t.

Higher credit scores generally mean that you can expect better terms, lower interest rates, low or no fees, signup bonuses, and other extras when applying for credit cards and borrowing money.

Credit card companies and other lenders will ask for income when you apply for new credit, which is where some of this confusion may come from.

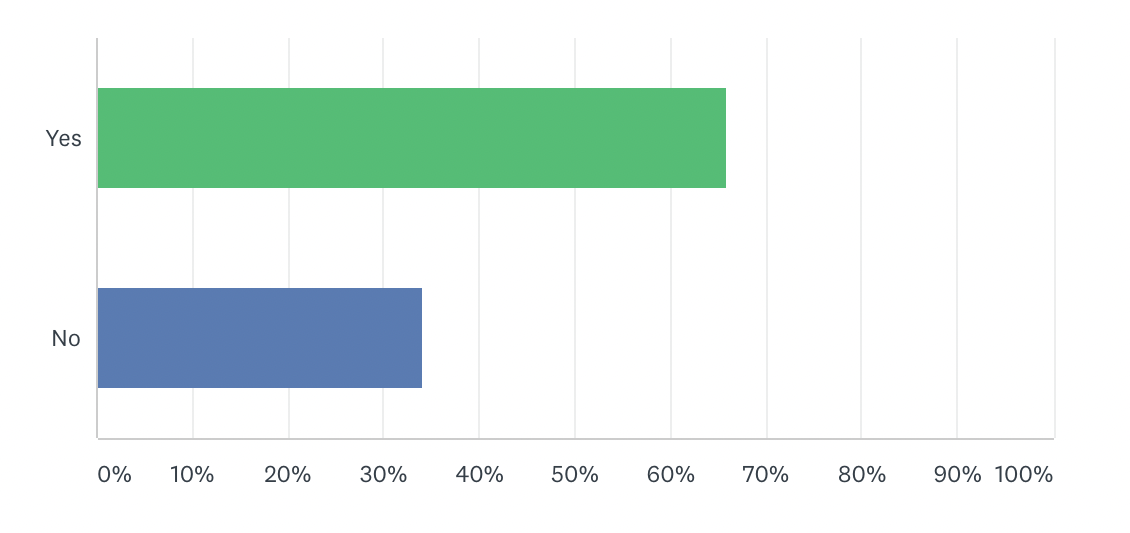

Do you think closing a credit card account is good for your credit scores?

- Yes: 28.44%

- No: 71.56%

Another common misconception is that once you pay off a credit card in full, closing the account is good for your credit scores. Twenty-eight percent of respondents thought this to be true. Similarly, 29% of those surveyed in 2019 thought the same.

But it’s not true.

When you close a credit card account, you may cause your credit utilization to go up, which wouldn’t be a good thing. Credit utilization is the ratio of your total balances to your total credit limits — the sum of your balances compared to the sum of your credit limits — and it’s one of the most important factors in your credit scores.

The lower your debt compared to your total credit limit, the better off you’ll be in this category. Closing a credit card will reduce your total credit limit, which would increase your utilization if you’re carrying any debt, and this could cause a sudden decrease in your credit scores.

Closing a card will also eventually affect your average age of accounts, but this isn’t as much of a concern. A card that was closed in positive status will remain on your credit reports for 10 years, adding to your average age of accounts the whole time.

Older accounts on your credit reports are better for credit scores. Unless the card has an annual fee you no longer want to pay, strongly consider keeping it open.

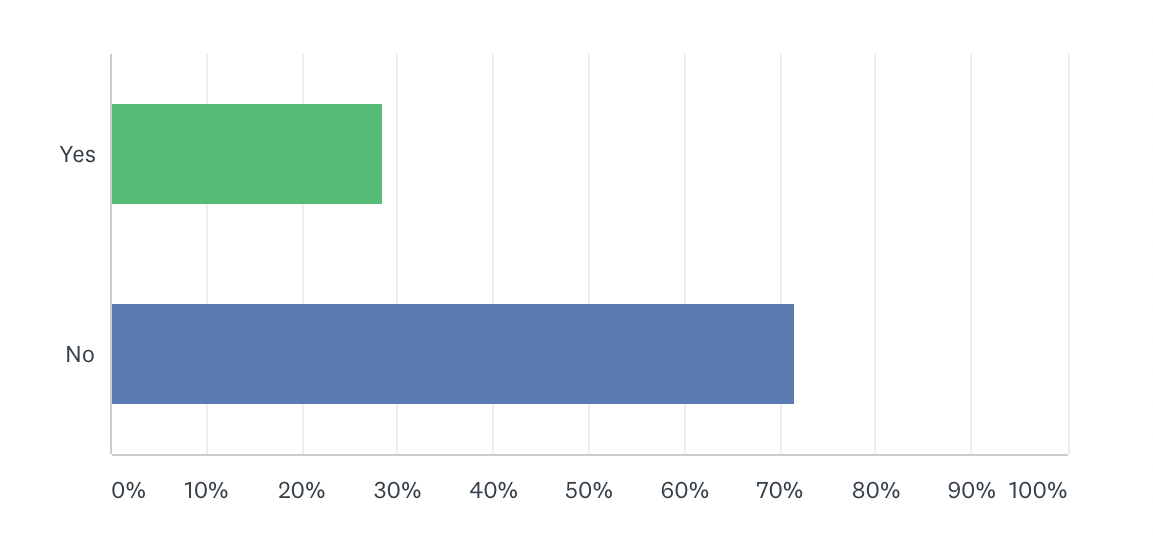

Do you think credit scores are included on your credit reports?

- Yes: 85.33%

- No: 14.67%

And then we have the biggest misconception, that your credit scores are included on your credit reports — they aren’t!

Eighty-five percent of all survey respondents were wrong, 6 percentage points more than those who guessed wrong in our 2019 survey!

Credit scores are based on the data in credit reports, but they’re not actually part of an official credit report. When ordering credit reports you can often pay extra to see your credit scores as well, but those scores aren’t technically part of your reports.

You should already be monitoring your credit reports to look for any fraudulent activity or inaccuracies. Since the COVID-19 pandemic, you can check all three of your credit reports for free once per week through April 2022 instead of the usual once per year.

If you want to get your FICO® credit scores for free too, it’s recommended to go through your credit card issuers. Many major card issuers, like American Express, Bank of America, Citi, and Discover offer free FICO® scores to their cardholders. Many others offer free VantageScores®, not only for cardholders but anyone who wants to sign up.

Most free services only give you access to one credit score, usually for just one of your credit reports. If you stack multiple free score services together, you can get a better idea of what credit range you stand in.

We recommend checking in on your credit scores several times per year, and whenever you plan to apply for any new credit.

Online Shopping and Payment Methods

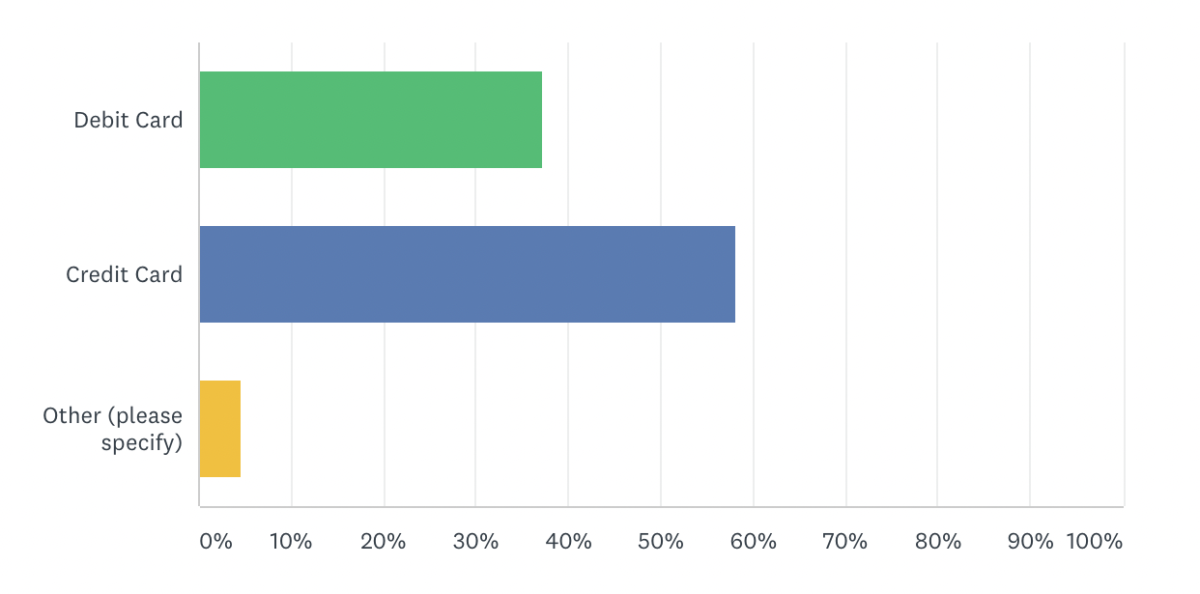

When shopping online, what payment method do you use most often?

- Debit Card: 37.32%

- Credit Card: 58.16%

- Other: 4.52%

Online shopping is very popular, with 95% of survey respondents claiming they shopped online since the start of 2020. This is likely due in part to people staying at home throughout the pandemic. When it comes to shopping online, how you choose to pay could be more rewarding and more secure depending on which payment option you choose.

Credit cards provide a number of advantages over debit cards, from credit building to convenience to security.

By using a credit card responsibly, you can build up a positive credit history while earning rewards when you shop. The Amazon Prime Rewards Visa Signature Card, for example, earns 5% back at Amazon.com, and offers an Amazon gift card upon approval.

Perhaps even more beneficial are the security features that come with credit cards.

Say you make an online purchase and your information gets compromised. When criminals fraudulently use your credit card, they’re spending your credit card issuer’s money, giving you time to report and manage the fraud before your bill is due. Consumer protection legislation, which includes laws like the Fair Credit Billing Act (FCBA), is generally stronger for credit cards than debit cards.

Debit cards usually don’t offer rewards, and don’t come with the same level of liability protection. When criminals fraudulently use your debit card, they’re spending money directly from your checking account, and depending on your bank, it could take weeks or months to get your money back. This could cause you to miss bill payments or force you to borrow money for daily expenses.

Of the almost 5% of respondents who said “Other,” most listed gift cards, prepaid cards, or PayPal as their preferred payment method.

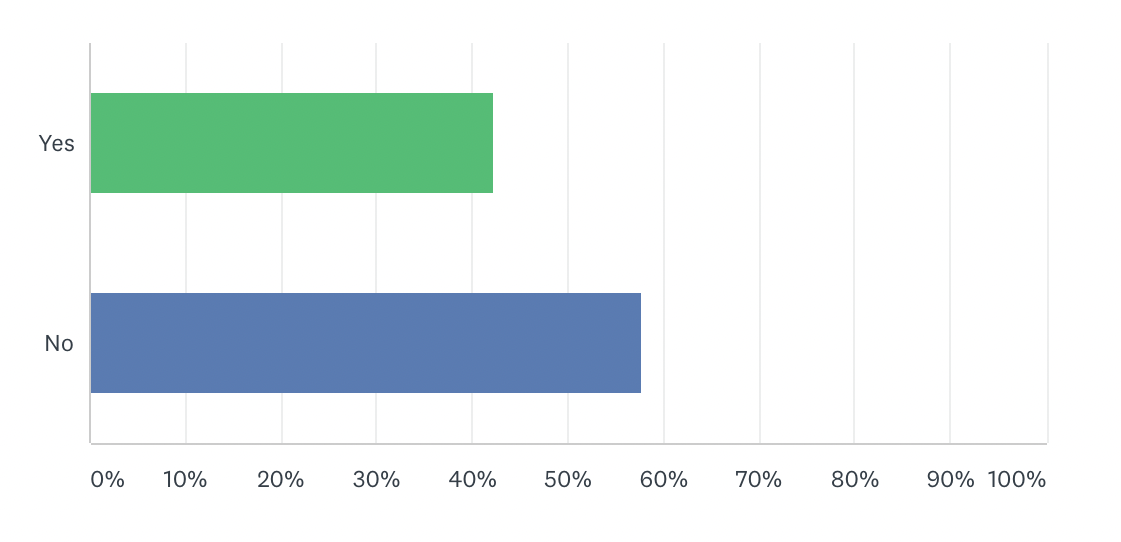

We asked survey respondents if they have ever made a payment using two of the most popular mobile wallets, and over 57% said that they haven’t.

Have you ever made a payment with Apple Pay or Google Pay?

- Yes: 42.25%

- No: 57.75%

There are some differences between mobile and digital wallets, but one key thing they have in common is an added layer of security when making purchases.

Through what is called tokenization, your payment information is encrypted in the form of a “token,” which allows payments to be processed without exposing your actual account numbers. The token is used for online payments, and for contactless payments when using a mobile wallet in-store.

Even if your token is stolen, the thief doesn’t have your real card details; the card company will simply issue a new token and your real card number will remain safe.

Mobile wallets require a passcode, fingerprint, or face scan before you’re able to complete a payment. This makes them more secure than credit cards or cash, and effectively adds that security to any payment method you store in them.

Wrapping Up

How comfortable do you feel when it comes to financial literacy? The good news is, answers to all of the common questions are out there. With a better understanding of how things really work, you can make better decisions to improve your own financial situation.

As we head into this year’s Financial Literacy Month, take a moment to reassess what you know (especially if you’re having trouble with debt), and take any steps necessary to get back on track.

Methodology

SurveyMonkey was commissioned to conduct this online survey of 2,015 adults over the age of 18 in the United States from March 15 – 17, 2021.

The Short Version

- Almost half of the survey respondents (47%) are currently paying interest on credit card debt

- On average, credit card interest rates are higher than on other types of debt

- Higher credit scores generally mean you can expect better terms, lower interest rates, and other extras when applying for credit cards and borrowing money